As of June 2024, Poland's electric vehicle (EV) market is demonstrating robust growth and increased infrastructure development, according to the latest data from the Polish EV Outlook Index (PEVO Index). This monthly report provides key statistics and insights into the e-mobility sector in Poland, revealing significant progress in electric vehicle adoption, charging infrastructure, and the secondary market for zero-emission vehicles.

Electric Vehicle Growth

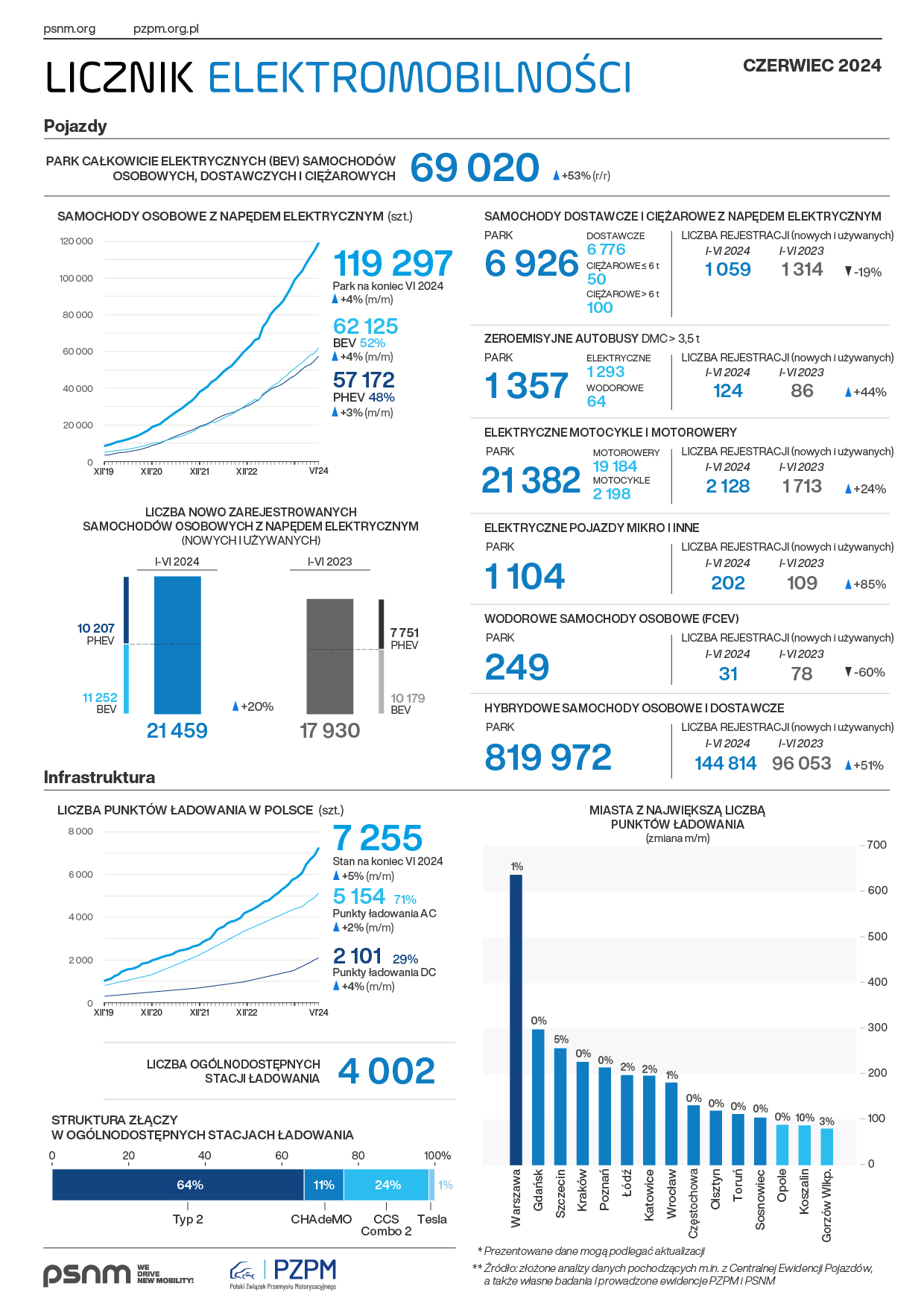

At the end of June 2024, Poland's fleet of battery electric vehicles (BEVs) for passenger, delivery, and heavy-duty vehicles totaled 68,792 units. This marks a substantial increase, with the passenger BEV fleet alone growing to 61,976 vehicles, a 54% rise compared to the previous year. In June 2024, there were 1,809 new BEV registrations, reflecting a 17% year-over-year increase. The fleet of fully electric delivery and heavy-duty vehicles also expanded to 6,816 units, a 57% year-over-year growth. Additionally, the fleet of hydrogen passenger vehicles (FCEV) reached 230 units, up 20% from the previous year.

The most popular new BEV models in June 2024 were:

- Tesla Model 3: 583 units sold

- Tesla Model Y: 250 units sold

- Volvo EX30: 134 units sold

Leading the brand rankings were Tesla, Mercedes-Benz, and Volkswagen, with BEVs accounting for 4.2% of the new passenger car market share in June 2024.

Charging Infrastructure Expansion

Poland's public charging infrastructure has also seen significant growth. By the end of June 2024, there were 7,255 public charging points, a 41% increase from the previous year. This includes 5,154 AC charging points (up 32% year-over-year) and 2,101 DC charging points (up 66% year-over-year). The majority of the charging infrastructure comprises chargers with a power output of up to 22 kW (62%), but the number of fast DC stations with power exceeding 50 kW is rapidly increasing, with 971 such devices available by the end of June 2024.

The cities with the most developed charging infrastructure include:

- Warsaw: 636 charging points

- Gdańsk: 297 charging points

- Szczecin: 256 charging points

- Kraków: 226 charging points

- Poznań: 214 charging points

The number of charging points along the TEN-T network reached 764 by the end of June 2024, representing a 26% increase from the previous year.

Secondary Market for Zero-Emission Vehicles

The PEVO Index also provides insights into the secondary market for e-mobility in Poland. By the end of June 2024, there were 4,492 used BEV listings on the OTOMOTO platform, marking a 57% increase from the previous year. BEV listings accounted for 1.1% of all used vehicle listings, with these offers making up 0.8% of all advertisement views on OTOMOTO.

The most popular used BEV models in the secondary market were:

- Nissan Leaf: 365 listings, average price 60,454 PLN

- BMW i3: 300 listings, average price 78,859 PLN

- Tesla Model 3: 186 listings, average price 133,799 PLN

Conclusion

The "Polish EV Outlook" offers the most comprehensive analysis of Poland's zero-emission transport market. For over five years, PSNM has provided a thorough overview of the electric vehicle market, charging infrastructure, EV buyer demographics, legislative changes, and the impact of e-mobility on the energy sector. The PEVO Index, released monthly, presents these key data points in an accessible infographic format, highlighting the dynamic growth and development of the Polish e-mobility landscape.

For more information on the full "Polish EV Outlook" report, visit Polishevoutlook.pl.

Source: