Part of EAFO’s Series on EV Market Trends Across Europe

🔔 Subscribe to our newsletter for the latest updates: Subscribe here

📢 Follow us on LinkedIn for more insights: EAFO LinkedIn

The Swiss automotive market experienced a challenging year in 2024, with new car registrations declining by 5% compared to 2023. A total of 239,535 new cars were registered in Switzerland and Liechtenstein, marking a decrease of 12,679 vehicles. The market remains significantly below pre-pandemic levels, which hovered around 300,000 annual registrations. Economic headwinds and unclear policy directions surrounding the expansion of e-mobility have negatively impacted demand for new vehicles.

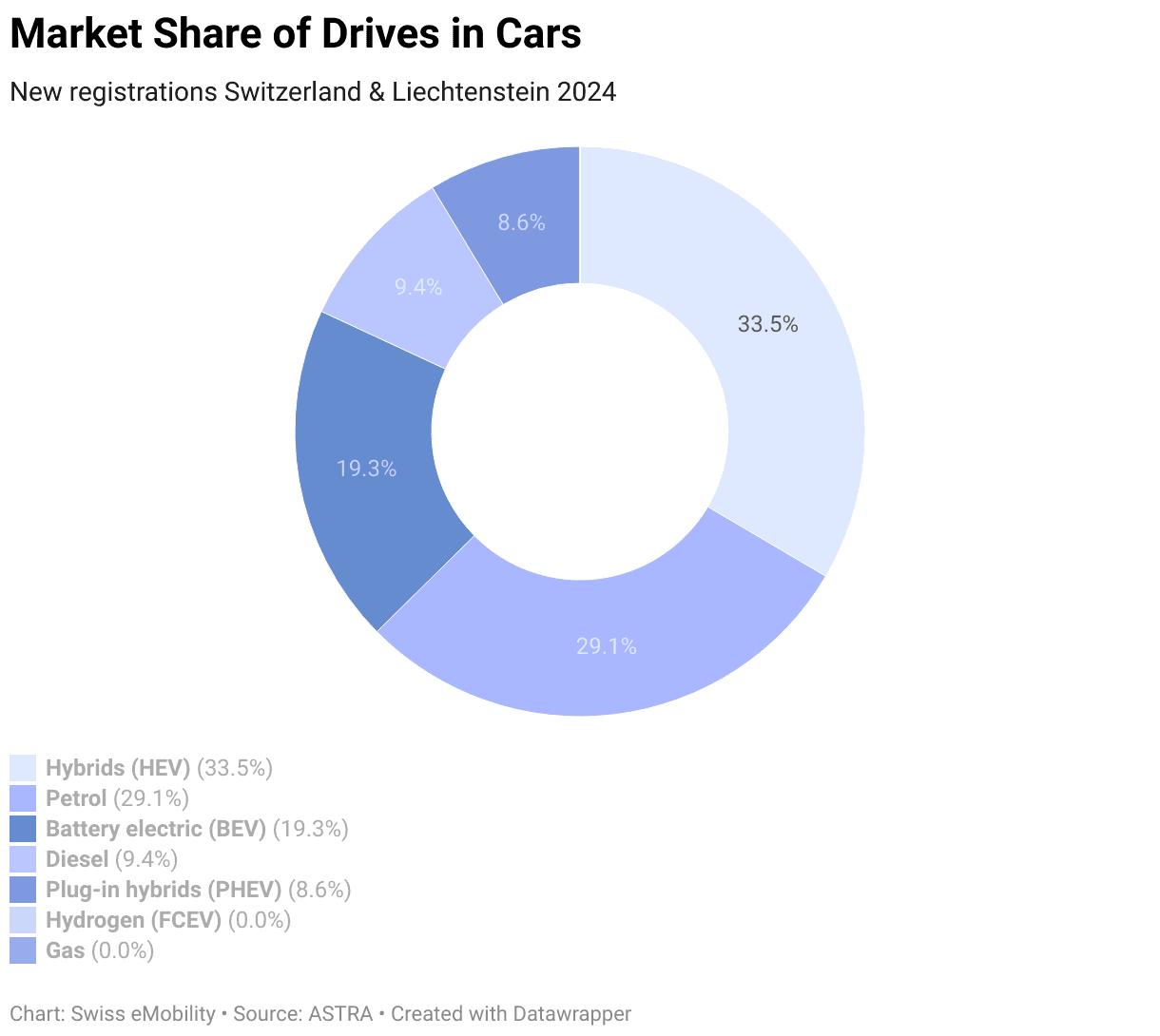

Despite growing demand for alternative powertrains, plug-in vehicles stagnated at a market share of 28%, failing to meet expectations. This comes at a time when stricter CO2 targets for cars and light commercial vehicles, along with new regulations for heavy-duty vehicles, are set to take effect in 2025, making a surge in electric vehicle (EV) adoption critical.

Plug-in Vehicles Stagnate, Hybrids Surge

Alternative powertrains reached a record 61.6% market share, with full and mild hybrids growing by 17%, now accounting for 33.6% of all new car registrations. However, battery electric vehicles (BEVs) and plug-in hybrids (PHEVs) saw declines of 12.5% and 10.4%, respectively.

This stagnation occurred despite the availability of more than 200 plug-in vehicle models on the Swiss market. Combined, plug-in vehicles accounted for 28% of the market, far below the 50% share needed to meet 2025’s new, stricter CO2 targets. Achieving these goals will require significant growth in the coming years.

Policy Failures Cited as Major Barrier

The decline in EV demand is largely attributed to policy missteps, including the reintroduction of a 4% import tax on electric vehicles at the start of 2024. This tax has increased the price of EVs, dampening demand. Additionally, the Swiss Parliament rejected strengthening private charging infrastructure under the revised CO2 Act, further complicating the e-mobility transition.

Peter Grünenfelder, President of auto-schweiz, stated:

"The 2024 results and slow EV adoption are the outcome of misguided policies. High electricity prices, unclear regulations, and a lack of incentives for private charging infrastructure have hindered progress. The government must focus on making the switch to e-mobility easier and more attractive for both individuals and businesses."

Adding to the uncertainty, Switzerland enters 2025 without clear regulations for implementing the new CO2 targets. According to auto-schweiz, the Federal Council is expected to clarify these rules only by mid-2025, leaving importers in a precarious position.

CO2 Target Compliance at Risk

With only 28% plug-in vehicles sold in 2024, the auto industry faces significant challenges in meeting 2025 CO2 reduction targets. According to Thomas Rücker, Director of auto-schweiz:

"We do not believe the current demand level for plug-in vehicles is sufficient to achieve 2025 CO2 targets. This applies not only to passenger cars but also to light commercial vehicles. Missing these targets could result in fines running into hundreds of millions of francs, costs that will inevitably be passed on to consumers."

Rücker called for measures to support EV adoption, including:

- Lower public charging tariffs and improved access to private charging stations.

- A suspension of the import tax on electric vehicles.

- Enhanced incentives for early vehicle replacements to accelerate fleet renewal.

Without these measures, Switzerland risks not only missing its environmental goals but also harming its third-largest import industry and the broader economy.

Regional Disparities and Best-Selling Models

EV adoption rates vary significantly across Switzerland. The highest EV shares were seen in Zurich (24.9%), Solothurn (24.1%), and St. Gallen (23.7%), while Ticino reported the lowest share at 11.2%.

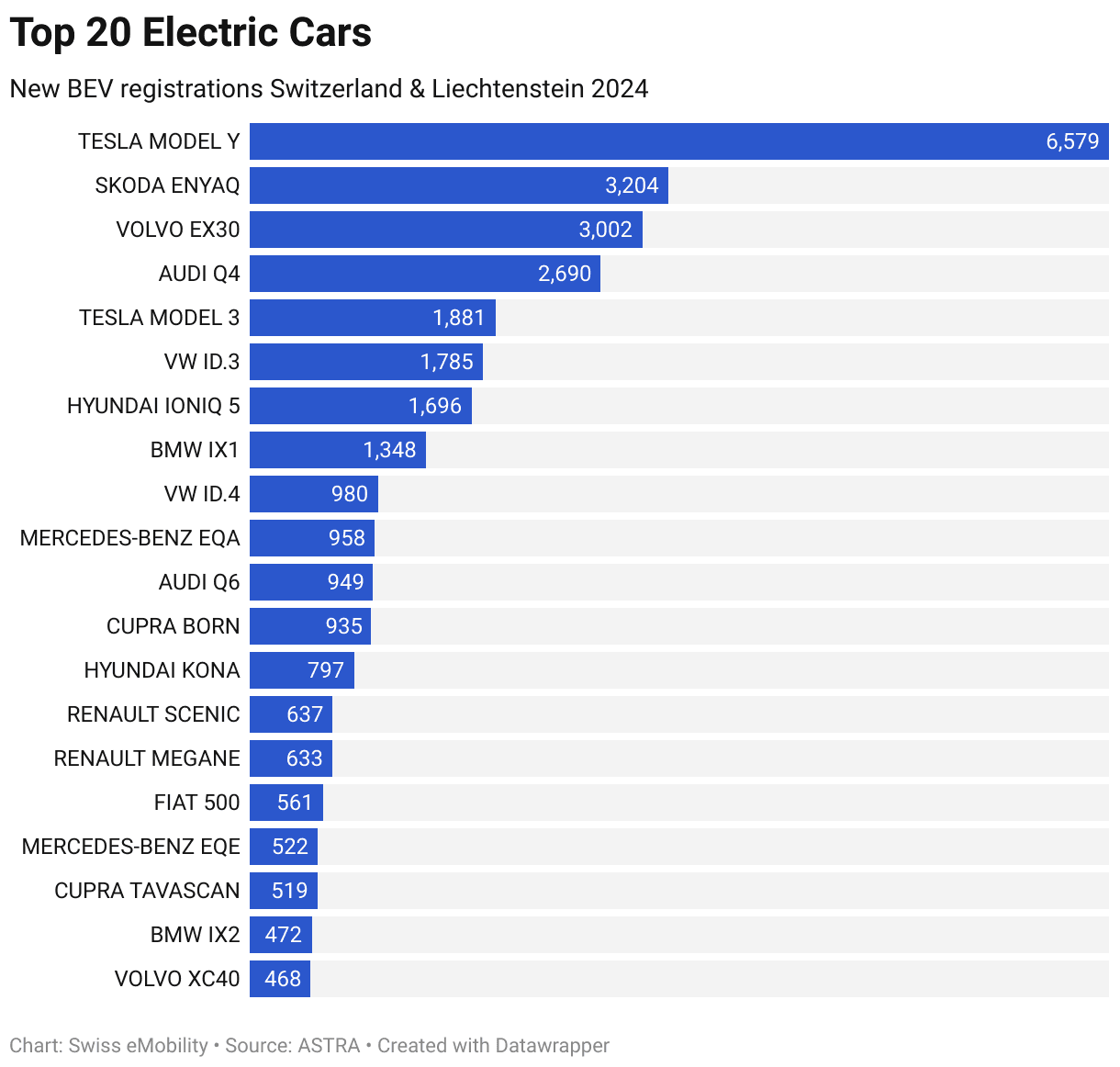

In terms of models, the Tesla Model Y remained the top-selling car overall, with over 6,500 units sold, followed by the Škoda Enyaq and Volvo EX30 among EVs. Large electric SUVs continue to dominate consumer preferences, reflecting a broader trend toward larger, more premium models.

Light Commercial Vehicles and Regulatory Challenges

The market for electric light commercial vehicles (e-LCVs) also faced hurdles, with their market share dropping to 8.1% (2023: 9%). Despite regulatory changes allowing electric vans to operate at weights up to 4.25 tonnes, unclear rules regarding road tolls and rest-time controls created uncertainty.

Toyota Proace was the best-selling e-LCV in 2024, followed by Renault Kangoo E-Tech and Renault Master E-Tech.

A Call to Action

To reverse the stagnation in e-mobility, industry stakeholders are recommending to adopt a more focused approach, including:

- Price reductions for EVs through tax relief.

- Expanded charging infrastructure with affordable tariffs.

- Clear and timely regulations to provide certainty for the industry and consumers.

Source:

Views and opinions expressed are those of the author(s) and do not reflect those of the European Commission.