In September 2024, the European automotive market saw a resurgence in electrified vehicle sales despite an overall market decline of 4% to 1.1 million units. Plug-in vehicles accounted for approximately 295,000 of those registrations, reflecting a 6% year-over-year (YoY) increase. This marks a return to growth for the EV market after months of stagnation. BEVs (battery electric vehicles) led the charge, showing a significant 14% growth to 212,000 units. However, PHEVs (plug-in hybrid electric vehicles) continued to struggle, experiencing a 9% decrease to 83,000 units.

Market Share and Powertrain Trends September's figures underscore a major shift in the European automotive landscape. Plug-in vehicles reached a 26% share of the overall market, with BEVs alone representing 19%. Coupled with HEVs (hybrid electric vehicles), which grew by 12% YoY and secured a 34% market share, a notable 60% of all new passenger cars sold featured some form of electrification. This is a significant milestone, indicating that more than half of new car buyers are opting for vehicles with at least partial electric capability.

The decline of traditional powertrains continued, with petrol vehicle sales falling by 19% and diesel slipping further by 24% to just 8% of the market. HEVs outsold petrol cars for the first time, capturing 34% of sales versus petrol's 29%. This trend suggests a permanent shift in consumer preferences and raises questions about the long-term viability of diesel and petrol in the European market.

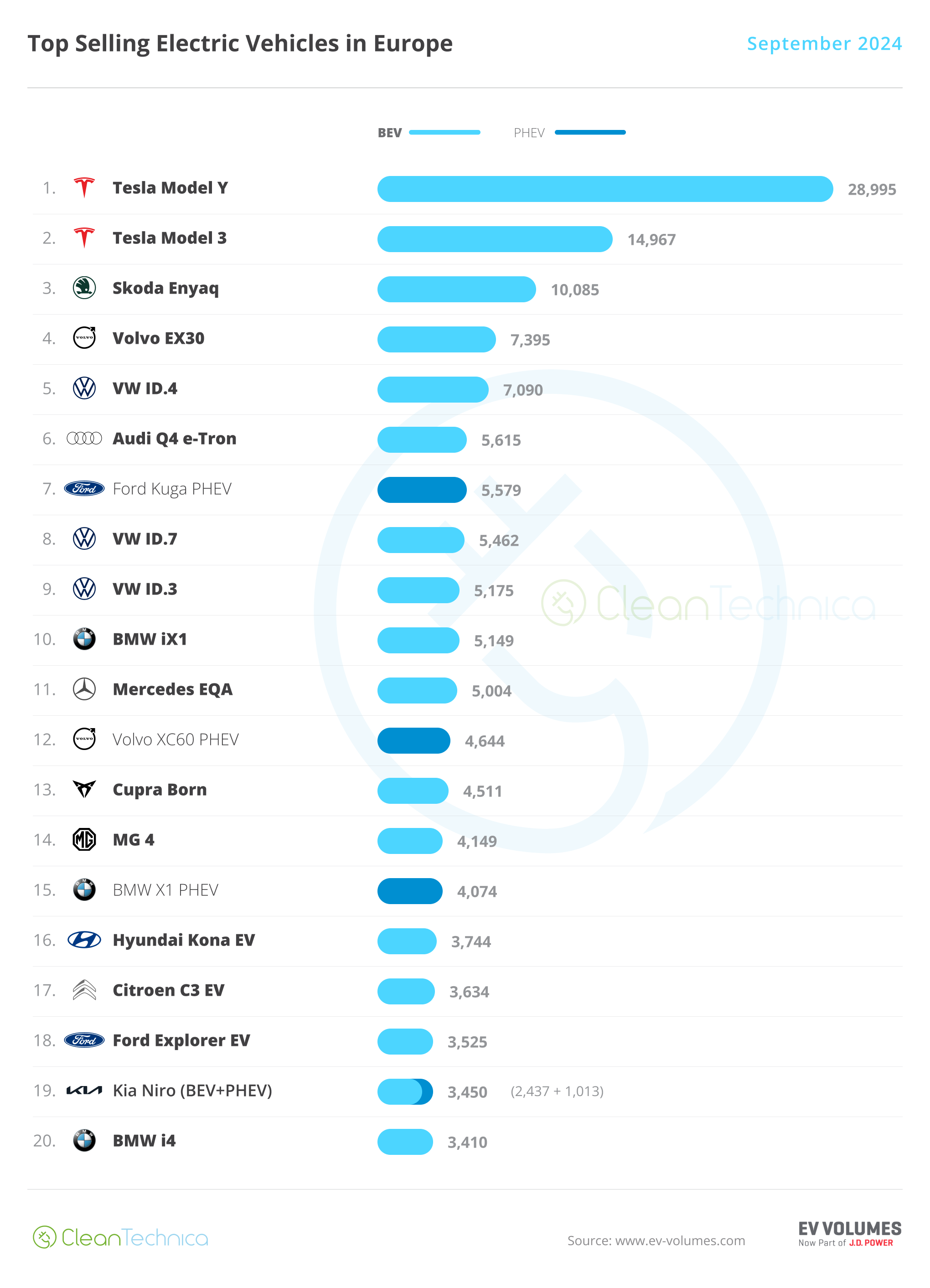

Top Electric Vehicle Performers #1 Tesla Model Y: Leading the European EV market once again, Tesla's Model Y recorded 28,995 registrations in September, maintaining its stronghold despite a slight 1% YoY drop. The UK remained the top market with 5,780 units, followed by France (4,591 units), and Sweden (4,125 units). The Model Y's dominance signals its continued appeal, even as Tesla prepares to introduce a refreshed version of its lineup.

#2 Tesla Model 3: Tesla's sedan saw an impressive performance, with 14,967 units sold — a threefold increase from the same period last year. This strong showing reinforces its position as Tesla's second-best model in Europe. Notably, the Model 3 was popular in Spain (2,221 units) and Italy (1,284 units), showcasing the region’s growing interest in sedan-style BEVs.

#3 Skoda Enyaq: The Skoda Enyaq posted a record 10,085 registrations, its first-ever five-digit monthly performance. This milestone, driven by its recent refresh, solidifies its place as a top competitor in the crossover segment. Germany led the way with 3,406 units, followed by the UK (1,520 units) and Norway (776 units).

#4 Volvo EX30: The Volvo EX30 continued to build momentum with 7,395 registrations. Although slightly impacted by new tariffs on China-made vehicles, it remains a strong performer, particularly in the UK (1,620 units) and the Netherlands (904 units). The EX30’s future performance will be closely watched as tariff implications unfold.

#5 VW ID.4: Volkswagen’s ID.4 climbed into the top five with 7,090 registrations, buoyed by recent updates to its specifications. While Germany was its largest market with 1,371 units, the UK led the month with 1,921 registrations, demonstrating the UK’s growing importance as an EV market.

Emerging Models and New Entrants Several new models showed promising results in September. The Citroën C3 EV made a notable debut with 3,634 registrations, securing the 16th spot on the monthly chart. If production scales smoothly, it could be a significant contender in 2025. Another newcomer, the Ford Explorer EV, reached 3,535 units, landing in the 18th spot in only its second month on the market.

Elsewhere, Volkswagen’s ID.7 continued to impress, recording its third consecutive monthly record with 5,462 registrations and making its first top 10 appearance at #8. The Mercedes EQA also set a personal best with 5,004 registrations, while the MG 4 re-entered the top 20, securing 4,149 sales.

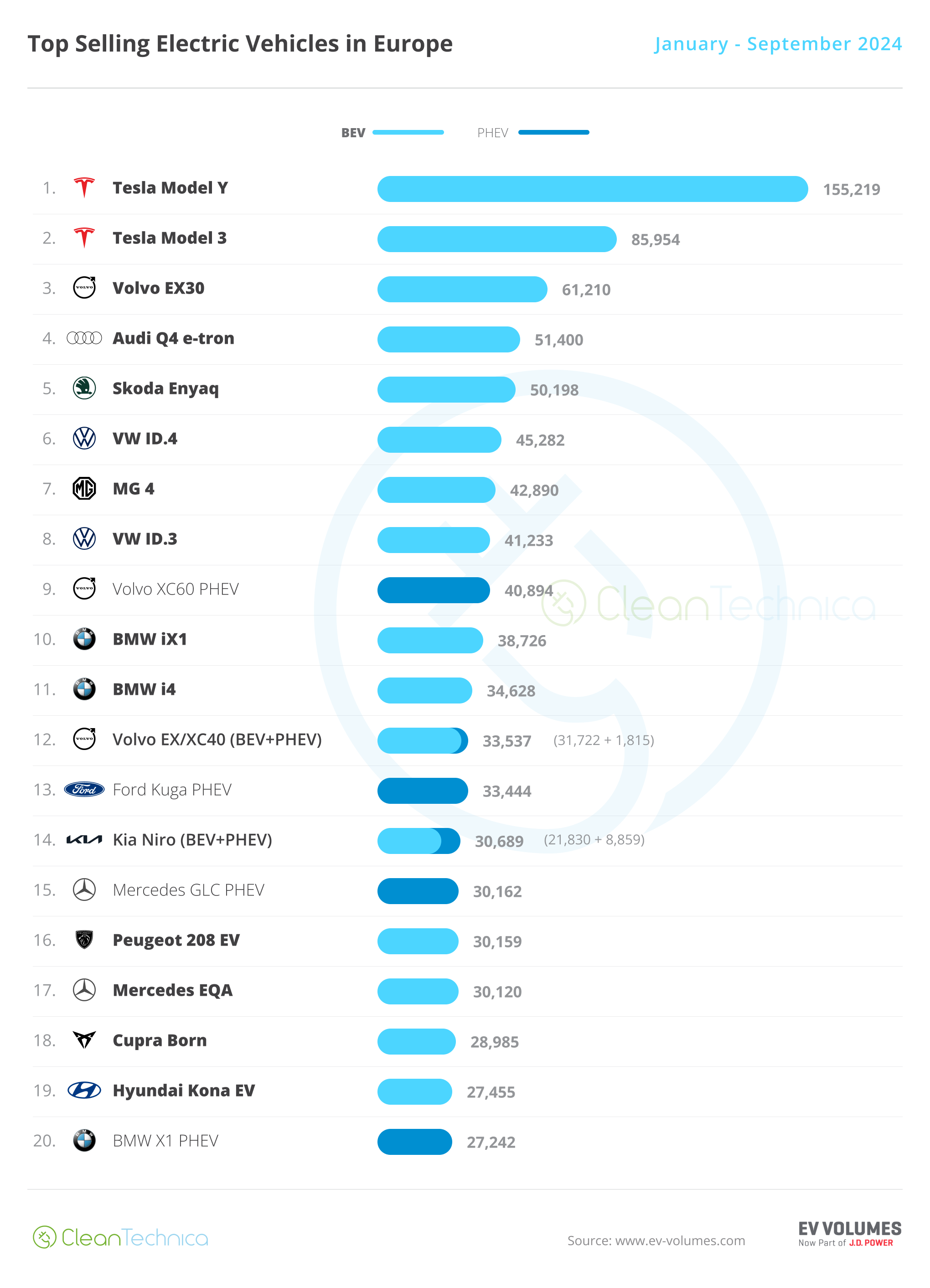

Market Dynamics and 2024 Outlook The Tesla Model Y holds a commanding lead in the 2024 year-to-date ranking, with a gap of 70,000 units over the Tesla Model 3, which is firmly in second place. With just three months left in the year, Tesla is on track to achieve a one-two finish for the third consecutive year. However, the competition for the third spot is more open, with the Volvo EX30 holding a 10,000-unit lead over its closest rivals, the Audi Q4 e-tron and Skoda Enyaq.

The bottom half of the top 20 saw the Hyundai Kona EV and BMW X1 PHEV rejoining the table at #19 and #20, respectively. This shake-up suggests that manufacturers are positioning their models strategically ahead of the stricter CO2 regulations set for 2025.

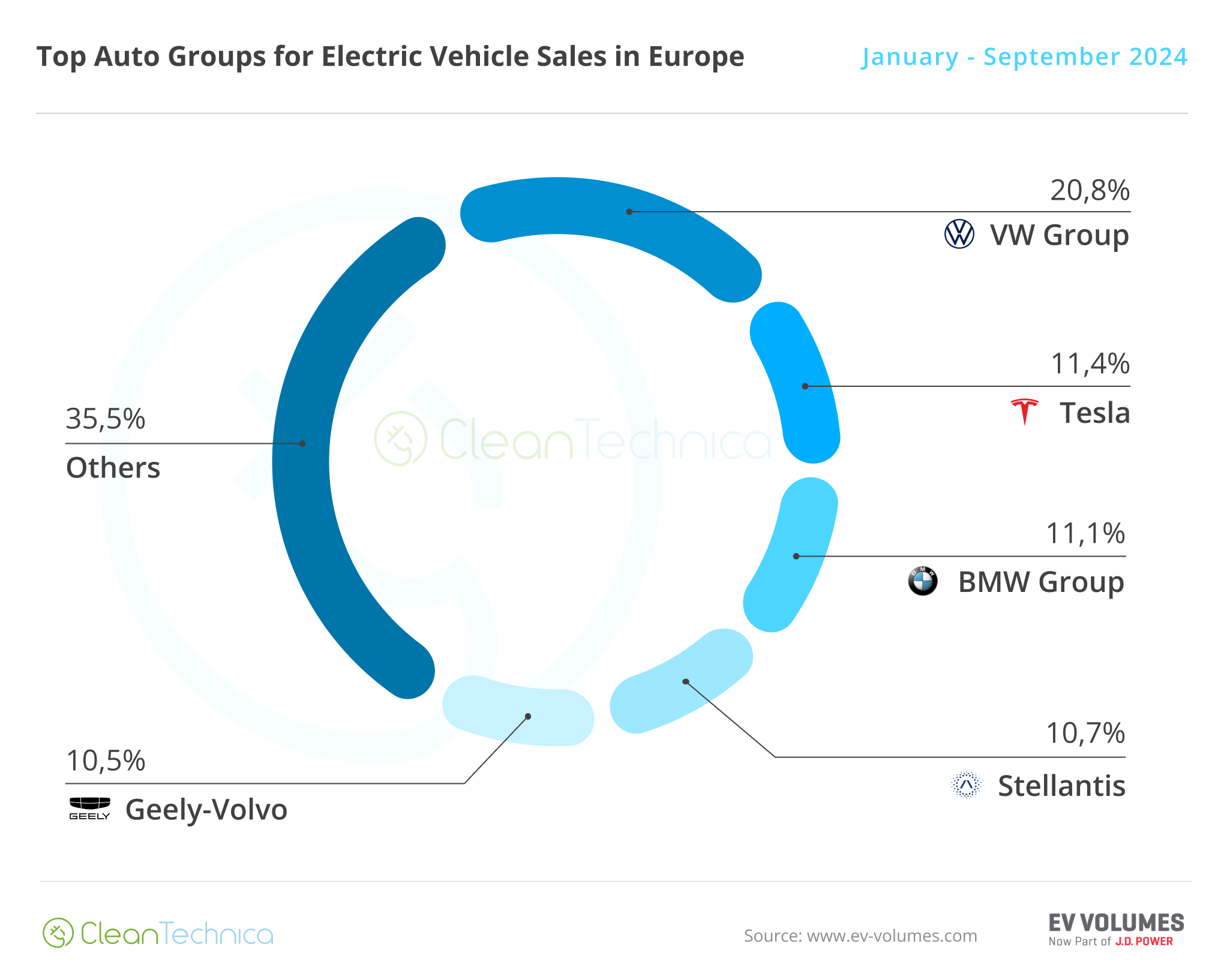

Brand and Group Performance Tesla remains the leading EV brand in Europe, with an 11.4% market share, followed by Volkswagen at 7%. While Tesla’s lead has narrowed compared to previous years, it is set to claim its third consecutive title. In terms of automotive groups, Volkswagen Group maintained its dominant position with a 20.8% market share, followed by Tesla at 11.4% and BMW Group at 11.1%.

As the European market continues its transition towards electrification, upcoming models and updates, coupled with regulatory pushes, will play crucial roles in shaping the landscape. The developments in 2025, particularly in response to new CO2 emission standards, are expected to further accelerate the move towards sustainable mobility.

Article by José Pontes, EAFO Team