Part of EAFO’s Series on EV Market Trends Across Europe

🔔 Subscribe to our newsletter for the latest updates: Subscribe here

📢 Follow us on LinkedIn for more insights: EAFO LinkedIn

Overview of December 2024

In 2024, 381,227 new passenger cars were registered in the Netherlands, a 3.1% increase compared to 2023. December saw an extraordinary surge, with 37,087 cars registered, marking a 40.3% increase compared to December 2023. This spike was largely driven by the anticipated end of consumer EV subsidies.

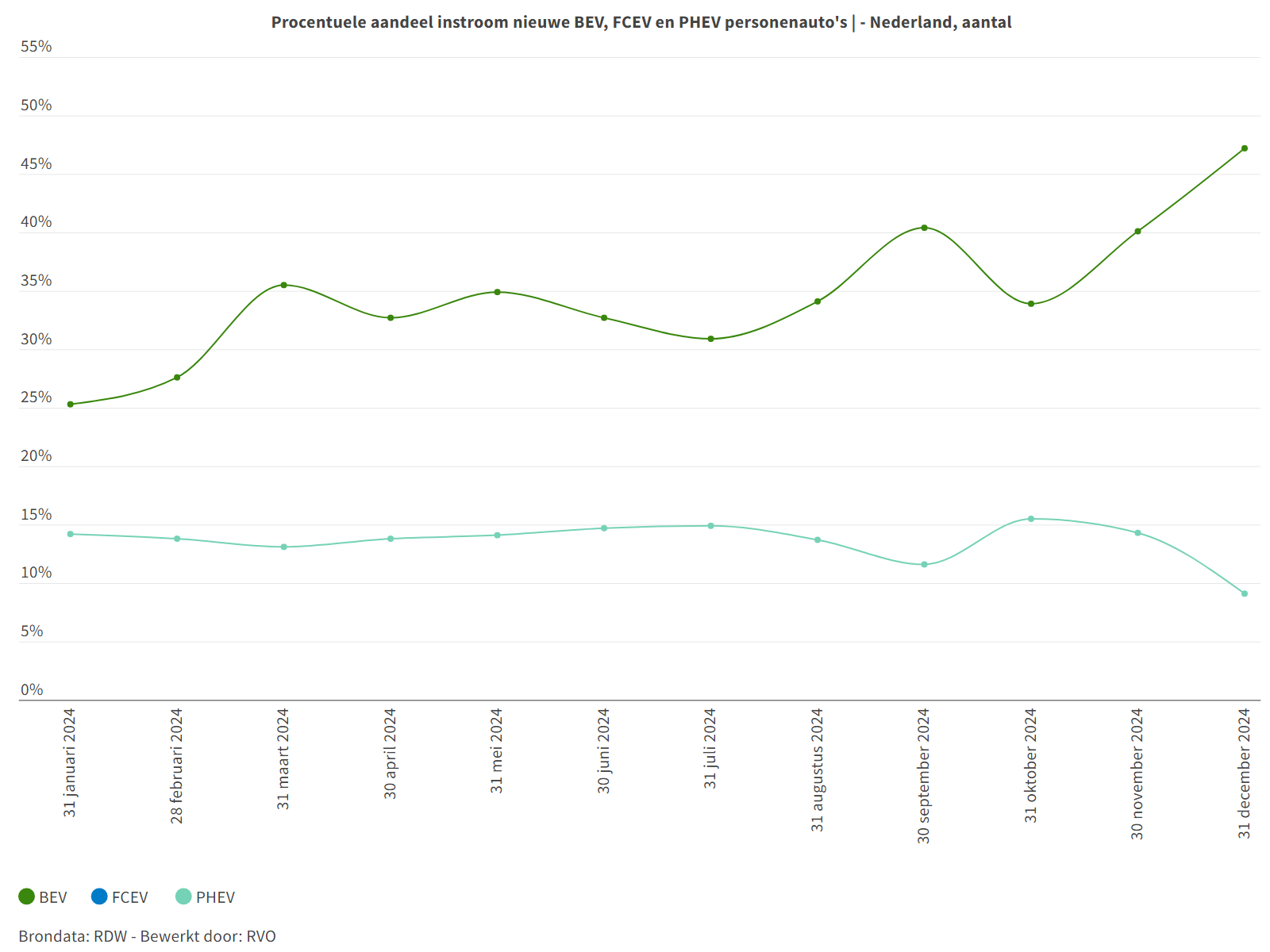

Monthly market share of BEVs, PHEVs and FCEVs in The Netherlands in 2024

Source: RVO

EVs and hybrids strengthened their position in the market:

- Hybrids: 159,705 registrations (41.9% market share, up from 37.1% in 2023).

- BEVs: 132,166 registrations (34.9% market share, up from 30.7% in 2023).

- Petrol vehicles: 83,408 registrations (21.9% market share, down from 30.4%).

- Diesel vehicles: 3,763 registrations (1.0% market share).

Despite the growth, the removal of the EV subsidy programme has cast uncertainty on future market trends, with no plans to reinstate grants for private EV purchases.

Key EV Models in 2024

The top EV models underscored Tesla's dominance, with the Tesla Model Y leading both the general and EV-specific market:

- Tesla Model Y: 19,058 registrations (14.4% EV market share).

- Volvo EX30: 10,802 registrations (8.2% EV market share).

- Tesla Model 3: 10,702 registrations (8.1% EV market share).

The Bigger Picture: Dutch Vehicle Fleet

Despite robust BEV sales, petrol-powered vehicles still dominate the broader vehicle fleet, comprising 75.1% of the 6.9 million passenger cars. However, BEVs now account for 6,1% of the passenger car fleet (557,671 vehicles).

The shift toward EVs has been largely propelled by the corporate sector, with 48% of all new registrations attributed to businesses. Notably, 55.9% of company cars were rechargeable (BEVs or PHEVs), demonstrating businesses’ significant role in fleet electrification.

The End of Incentives and Market Adjustments

In November 2024, the new EV grant fund was depleted, with similar exhaustion of funding for used EVs by December. This drove a December sales spike, reminiscent of patterns seen in Germany and Sweden after subsidy reductions. In 2025, the market faces additional challenges with the phased reduction of BEV road tax exemptions, which drop from 100% in 2024 to 75% in 2025, and 25% in 2026.

Growth in Light Commercial Vehicles

The light commercial vehicle (LCV) segment saw explosive growth, with 129,878 registrations (an 87.4% increase YoY), attributed to the end of BPM exemptions for combustion-engine vans and the introduction of zero-emission zones in city centers.

Looking Ahead to 2025

The Dutch EV market enters a transformative phase as it adapts to reduced subsidies. Key factors influencing the future include:

- Second-hand EV Market: Growing availability of affordable corporate lease returns.

- Charging Infrastructure: The Netherlands remains a leader with over 157,000 recharging points.

- EU Regulations: Manufacturer penalties for emissions are likely to continue driving EV adoption.

Industry leaders, like BOVAG, stress the importance of long-term regulatory stability to ensure consistent growth in the EV sector, with a focus on maintaining affordability and accessibility for consumers.

Top Takeaway

2024 marked a transitional year for the Netherlands, with steady growth in EV adoption despite subsidy phase-outs. The shift underscores the need for robust secondary markets and supportive fiscal policies to sustain momentum in electrifying Dutch mobility.

Source:

Views and opinions expressed are those of the author(s) and do not reflect those of the European Commission.